S&P 500 6,591.90 (+0.5%) · 10Y Treasury Yield 4.33% (-6bps) · Gold $4,503.30 (+$104.00 (+2.4%)) · VIX 25.33 (-6.0%)

Subscribe

·

How It Works

·

Archive

Daily Market Brief

Wednesday, March 25th, 2026

The 56 Maple Daily Brief is a curated macro and markets summary built for private equity investors and operators.

It tracks 40+ key indicators across rates, credit, equities, currencies, commodities, flows, and real estate. Highlighting what moved and why.

Delivered each day with AI-powered interpretation and relevant analysis via the lastest Anthropic Model.

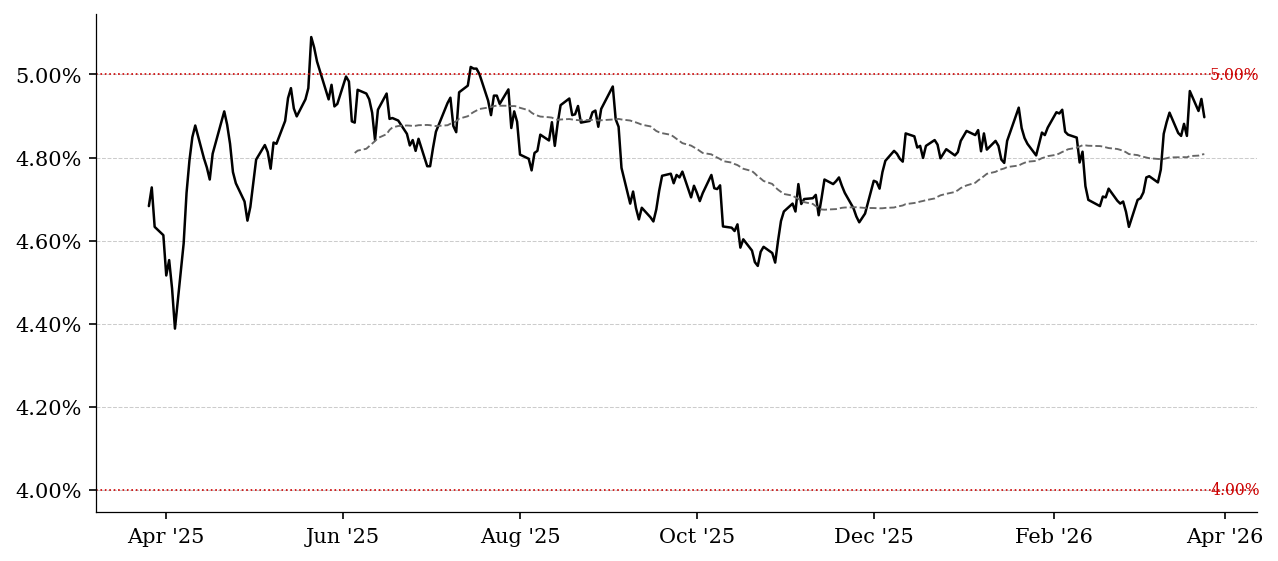

10Y Treasury Yield

4.33%

-6bps

Crude Oil (WTI)

$91.29

$-1.06 (-1.1%)

Gold

$4,503.30

+$104.00 (+2.4%)

Macro Interpretation

AI-generated synthesis · claude-sonnet-4-20250514 · Wednesday, March 25th, 2026

Bonds

The curve steepened with 5Y and 10Y yields rising 11bp and 7bp respectively over the past week while the 2Y held steady. Real rates surged 13bp in the past week to 2.06%, while breakeven inflation expectations fell across the curve, suggesting the market is pricing in tighter monetary conditions rather than growth concerns. The 2s10s spread compressed to just 49bp, down from much steeper levels earlier in the year. Conviction: HIGH.

Credit

High yield spreads held stable over the past week despite the backup in rates, with both HYG and LQD showing resilience. The HY spread at 3.19% remains contained, suggesting credit markets are not signaling stress despite the rate volatility. This divergence between rising rates and stable credit suggests the bond selloff is driven by growth or inflation concerns rather than credit quality deterioration. Conviction: MODERATE.

Private Credit

BDCs continue to underperform with BIZD down 0.7% and OBDC down 1.4% over the past week, extending YTD losses to over 10% for both. Senior loans showed slight strength with both BKLN and SRLN up modestly, indicating the leveraged loan market remains more resilient than direct lending vehicles. The persistent weakness in BDCs versus stable loan pricing suggests investors are pricing in margin compression and potential credit losses in the direct lending space. Conviction: HIGH.

Equities

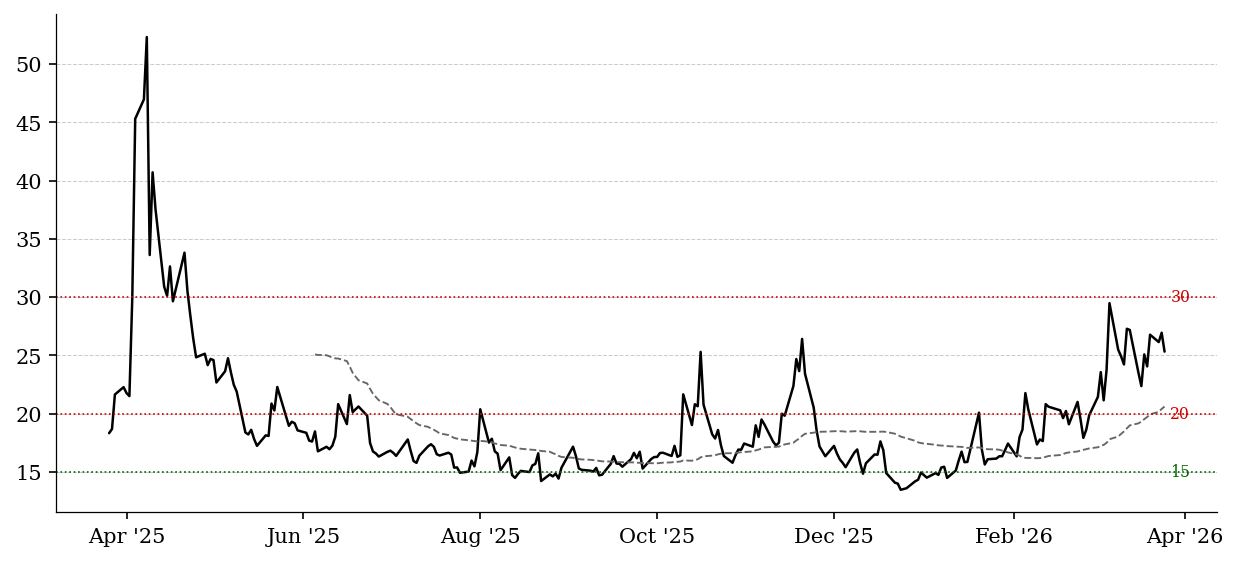

Small caps outperformed with Russell 2000 up 2.3% over the past week while large caps remained under pressure, with the S&P 500 down 0.5%. The VIX remains elevated at 25.33, up 74% YTD, indicating persistent uncertainty. Equal weight performance matching cap-weighted suggests broad-based participation in any rallies, but the month-long decline across all major indices points to underlying weakness. Conviction: MODERATE.

Commodities

Oil continued its sharp retreat, falling 5.2% over the past week despite remaining up 39% over the month, suggesting recent gains may have been overdone. Gold fell dramatically, down 7.9% for the week and 12.7% for the month, indicating a significant shift in risk appetite and dollar strength. Copper remained stable, providing mixed signals on global growth expectations. Conviction: MODERATE.

Real Estate

REITs fell sharply with VNQ down 3.5% over the past week and homebuilders down 14% over the month despite recent strength. The 30Y mortgage rate rose to 6.22%, creating significant headwinds for housing demand despite strong housing starts data. The sector is being pressured by the combination of higher rates and valuation concerns. Conviction: HIGH.

Today's Environment

Transition regime. Rising real rates with stable credit spreads and mixed equity performance suggests markets are processing conflicting signals about growth, inflation, and Fed policy. The dramatic gold selloff and BDC weakness point to tightening financial conditions, while stable loan markets and contained credit spreads suggest the system remains functional.

Practical Investment Implications

Favor floating rate assets and senior loans over fixed rate credit given the rate environment. Avoid duration risk and BDCs until the direct lending cycle shows signs of stabilizing. The combination of rising real rates and falling breakevens creates opportunities in TIPS and short-duration strategies.

One Key Change to Watch

A sustained move in high yield spreads above 350bp would signal transition from rate-driven to credit-driven stress.

Bonds

2Y Treasury Yield

^IRX

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 3.62% |

+0bps |

+1bps |

+3bps |

+9bps |

As of March 25, 2026

Yield on short-term U.S. government debt, primarily driven by expectations for Federal Reserve policy over the next 1-2 years.

This is the market's real-time view of where the Fed is headed; when it rises, the market is pricing tighter policy or delayed cuts, and when it falls, it reflects expectations of easing or economic slowdown, making it one of the most important forward-looking policy indicators.

5Y Treasury Yield

^FVX

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 3.97% |

-6bps |

+11bps |

+37bps |

+23bps |

As of March 25, 2026

Intermediate-term Treasury yield that reflects both expected Fed policy and medium-term economic conditions.

This sits between short-term policy and long-term growth expectations, so changes here often signal a shift in the market's base-case economic outlook rather than just near-term Fed moves.

10Y Treasury Yield

^TNX

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 4.33% |

-6bps |

+7bps |

+30bps |

+14bps |

As of March 25, 2026

Benchmark long-term interest rate reflecting expectations for growth, inflation, and risk over a full economic cycle.

This is the most important rate for asset pricing; rising yields generally indicate stronger growth or higher inflation expectations and tighten financial conditions, while falling yields signal slowing growth, disinflation, or risk aversion, directly impacting valuations across equities and real estate.

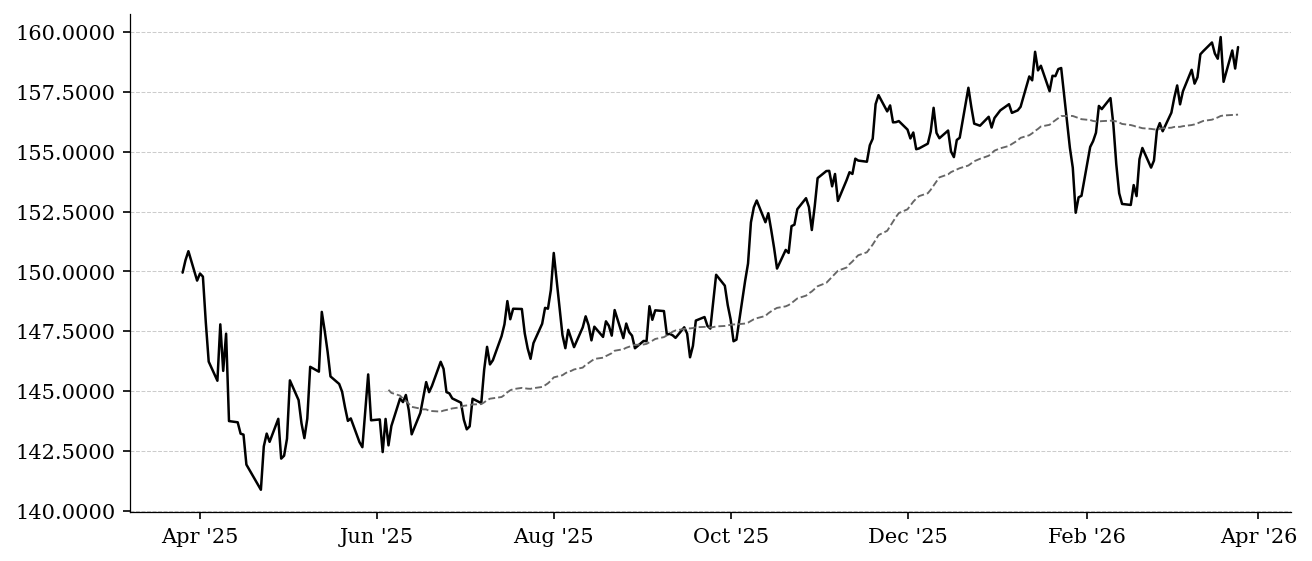

30Y Treasury Yield

^TYX

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 4.90% |

-0.9% |

+0.3% |

+4.4% |

+0.7% |

As of March 25, 2026

Long-duration yield reflecting long-term economic expectations, inflation risk, and fiscal sustainability.

Movements here are less about near-term cycles and more about structural views on inflation and government debt, making it particularly relevant for long-duration assets and understanding long-term capital costs.

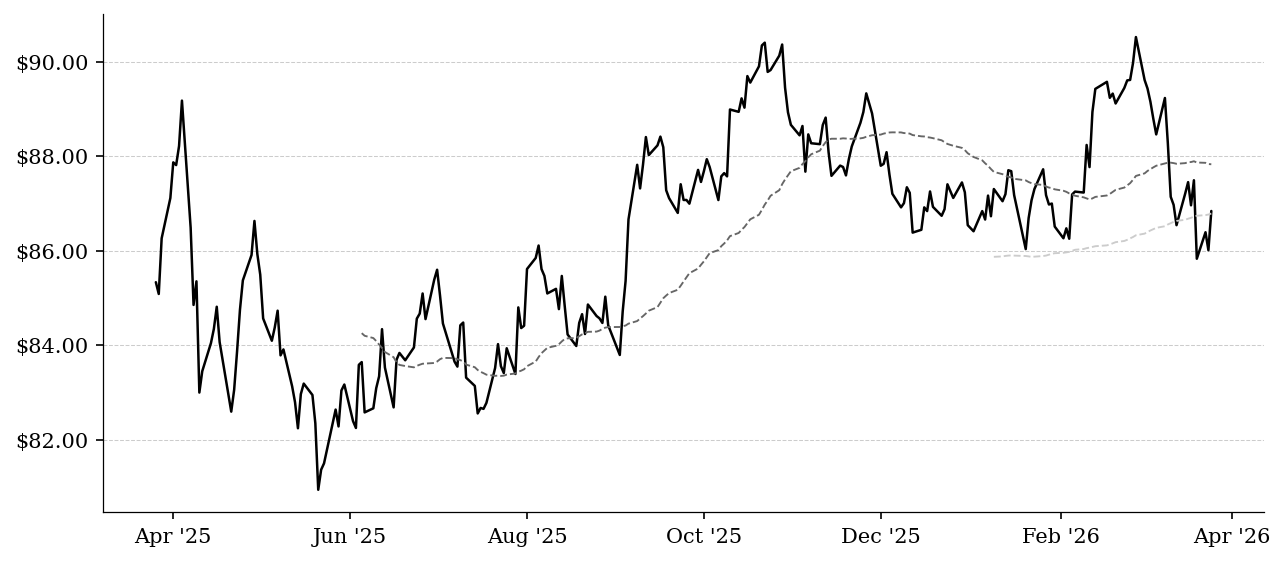

20+ Year Treasury Bond ETF

TLT

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $86.84 |

+$0.83 (+1.0%) |

$-0.12 (-0.1%) |

$-2.76 (-3.1%) |

+$0.43 (+0.5%) |

As of March 25, 2026

ETF representing long-duration U.S. Treasury bonds, inversely related to long-term yields.

This acts as a real-time proxy for long-duration risk; when TLT falls, it indicates rising long-term rates and tightening financial conditions, and when it rises, it reflects declining yields and easing conditions, often coinciding with risk-off environments.

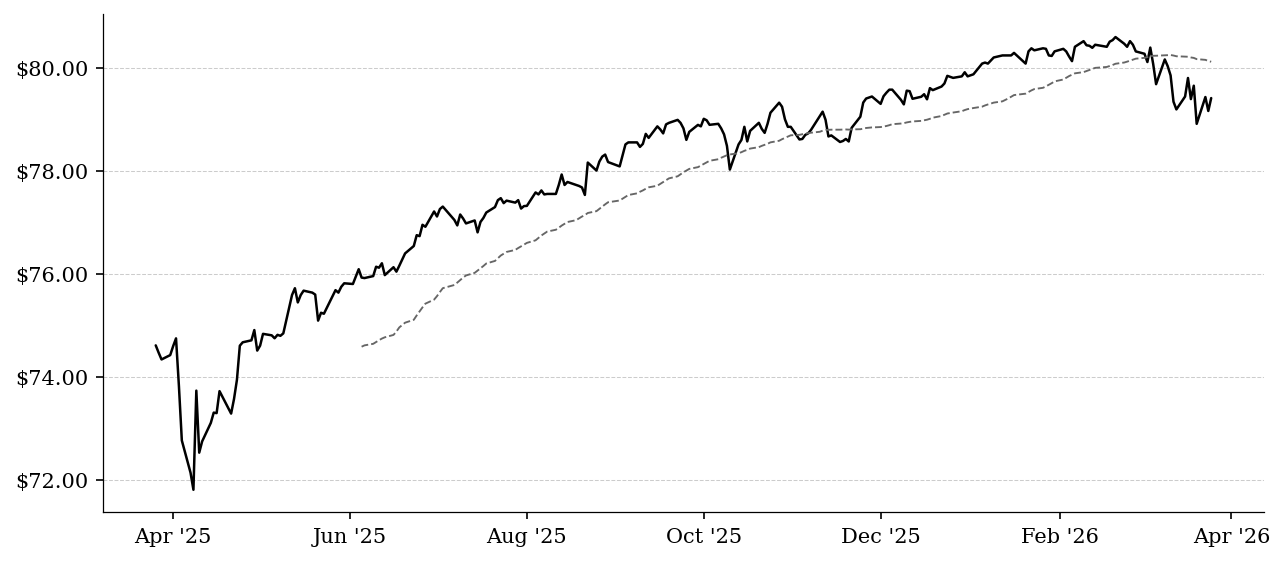

High Yield Corporate Bond ETF

HYG

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $79.42 |

+$0.25 (+0.3%) |

+$0.02 (+0.0%) |

$-1.00 (-1.2%) |

$-0.46 (-0.6%) |

As of March 25, 2026

ETF representing below-investment-grade corporate debt, combining credit risk and interest rate exposure.

This is a key proxy for credit risk appetite; rising prices suggest easy financial conditions and strong risk tolerance, while falling prices indicate widening credit spreads and increasing concern about defaults or economic stress.

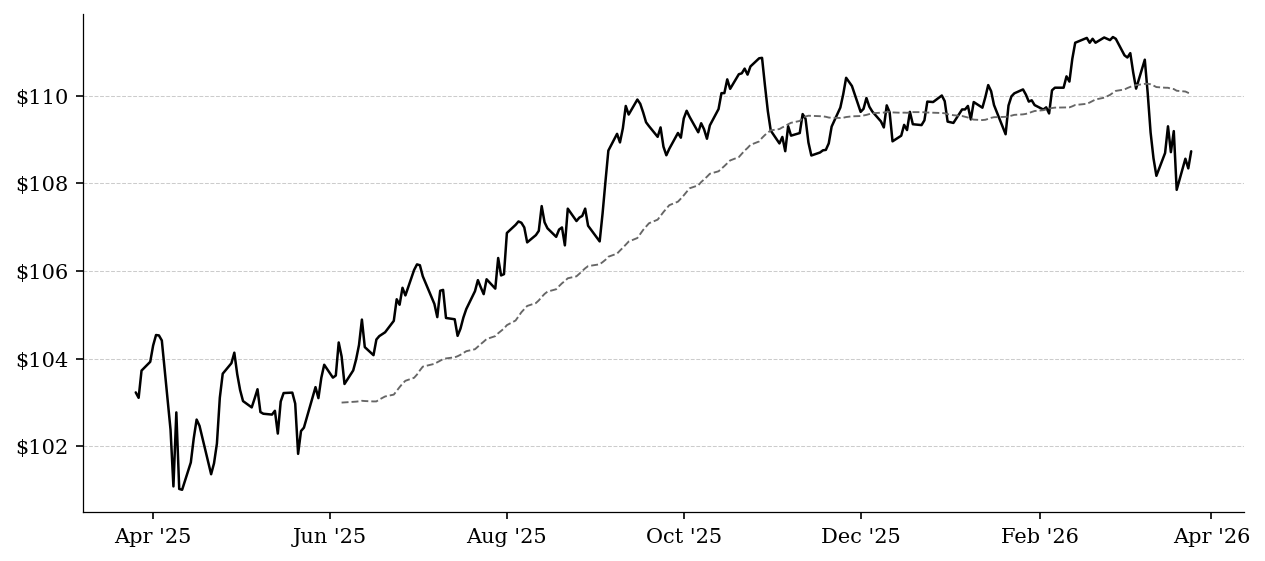

Investment Grade Corporate Bond ETF

LQD

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $108.73 |

+$0.39 (+0.4%) |

+$0.02 (+0.0%) |

$-2.57 (-2.3%) |

$-0.65 (-0.6%) |

As of March 25, 2026

ETF representing high-quality corporate bonds with lower credit risk than high yield.

This reflects both interest rate movements and corporate credit quality; weakness here can signal tightening financial conditions even before equity markets react, particularly if driven by spread widening rather than rates.

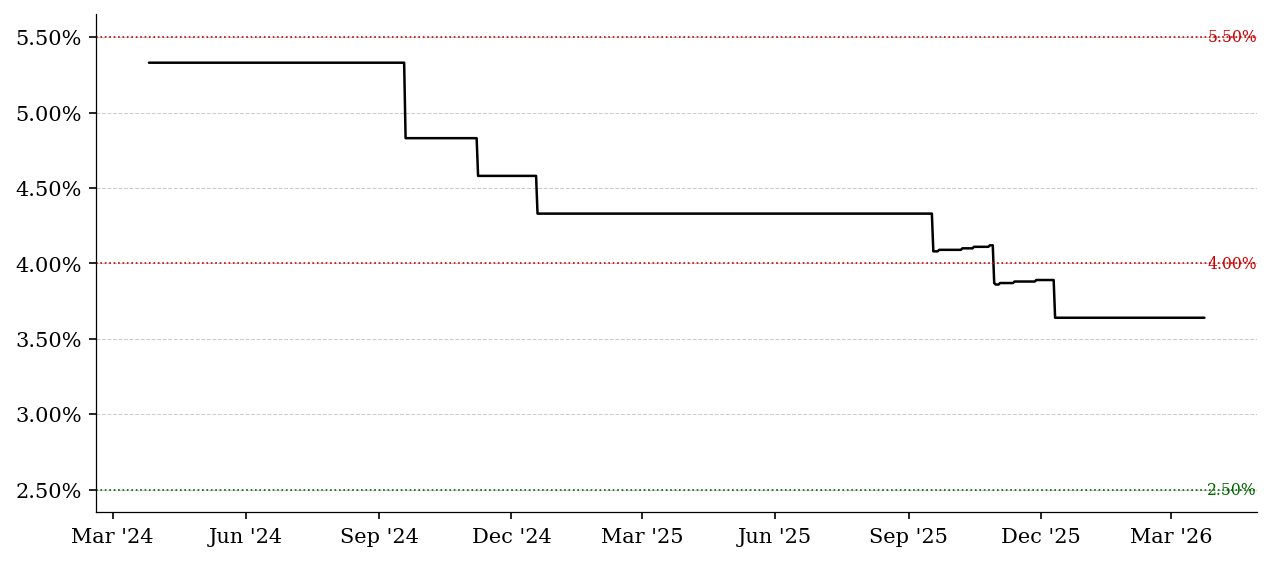

Fed Funds Effective Rate

DFF

· FRED

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 3.64% |

+0.0% |

+0.0% |

+0.0% |

+0.0% |

As of March 24, 2026

The actual overnight rate at which banks lend reserves to each other, reflecting current Fed policy.

This is the anchor of the entire rate system; changes here directly influence borrowing costs across the economy and serve as the baseline against which all other yields are evaluated.

2s10s Yield Curve Spread

T10Y2Y

· FRED

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 0.49% |

+0.0% |

-2.0% |

-19.7% |

-31.9% |

As of March 25, 2026

Difference between 10-year and 2-year Treasury yields, measuring the slope of the yield curve.

This is a core economic signal; an inverted curve (negative spread) suggests restrictive policy and elevated recession risk, while a steepening curve typically reflects either improving growth expectations or easing financial conditions.

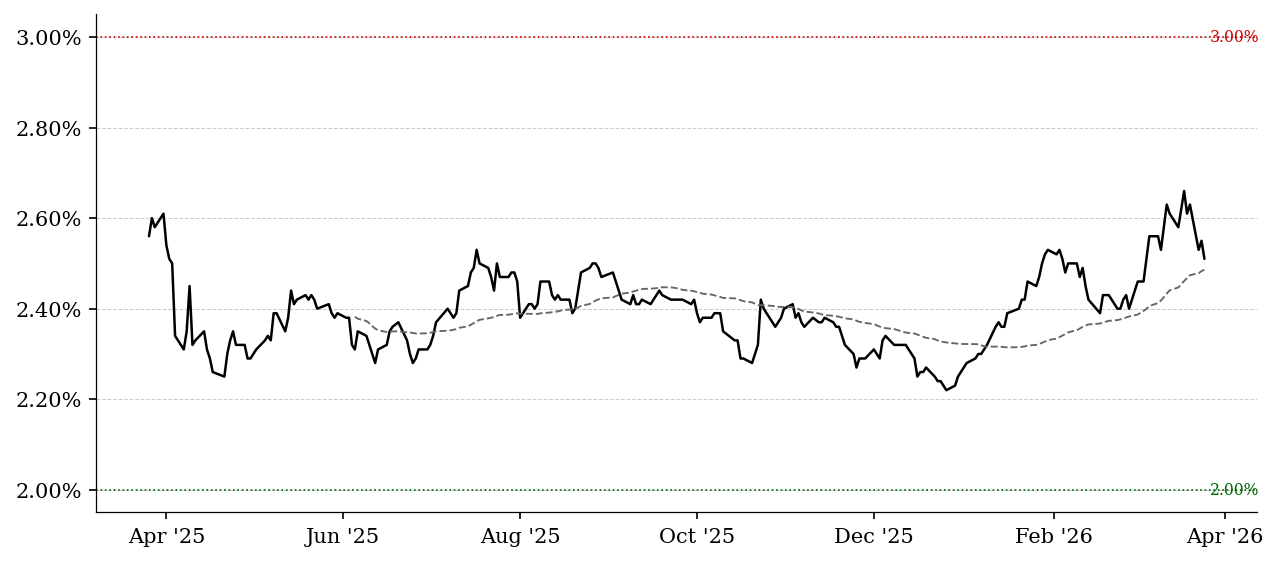

5Y Breakeven Inflation

T5YIE

· FRED

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 2.51% |

-1.6% |

-5.6% |

+4.6% |

+10.1% |

As of March 25, 2026

Market-implied average inflation over the next 5 years derived from nominal vs TIPS yields.

This reflects near-to-medium-term inflation expectations; rising breakevens indicate increasing inflation expectations, while falling breakevens suggest disinflation or weakening demand.

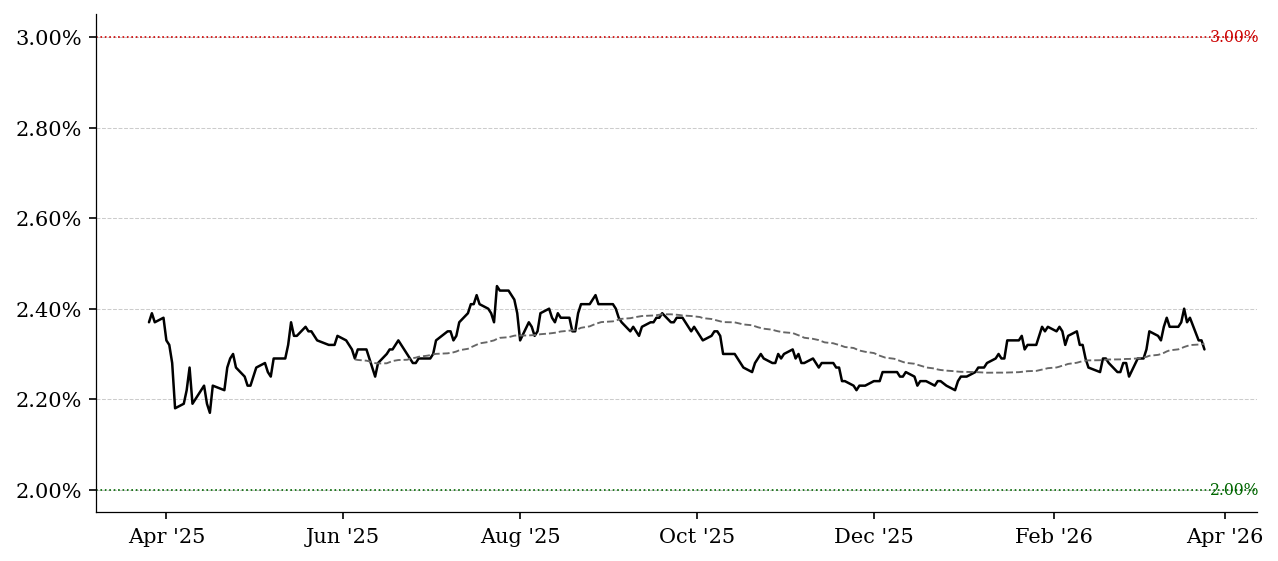

10Y Breakeven Inflation

T10YIE

· FRED

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 2.31% |

-0.9% |

-3.7% |

+2.2% |

+2.7% |

As of March 25, 2026

Market-implied inflation expectations over the next 10 years.

This provides a longer-term view of inflation credibility; stable levels suggest anchored expectations, while large moves signal shifts in confidence around long-term price stability.

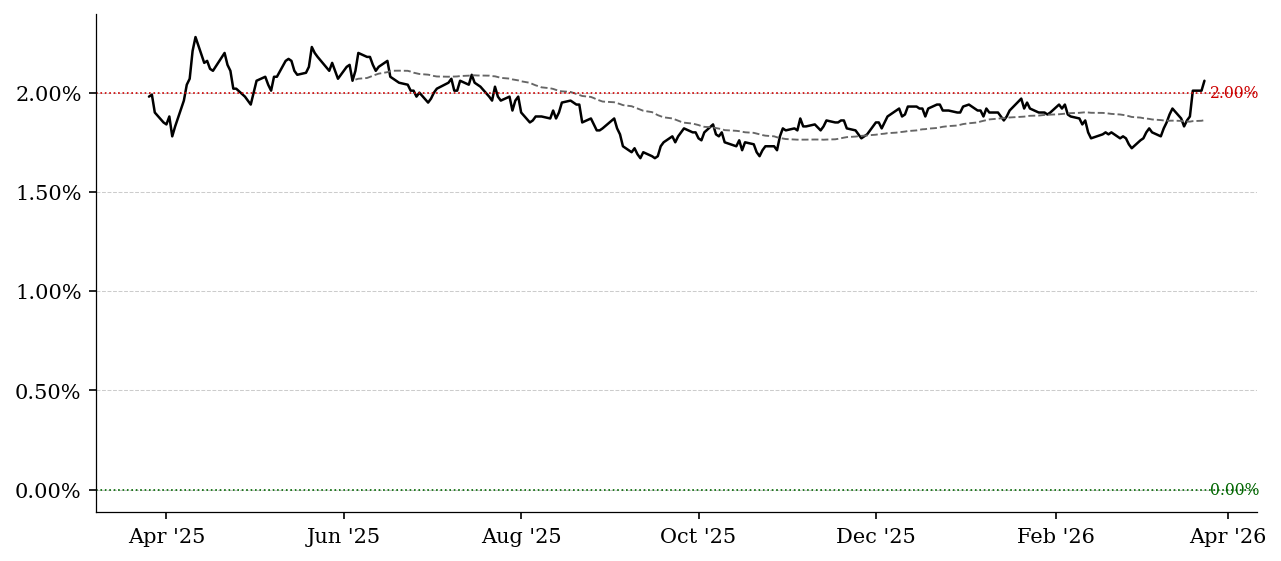

10Y Real Rate (TIPS)

DFII10

· FRED

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 2.06% |

+2.5% |

+12.6% |

+16.4% |

+6.2% |

As of March 24, 2026

Inflation-adjusted yield on 10-year Treasuries, representing the real cost of capital.

This is one of the most important variables for asset valuation; rising real rates tighten financial conditions and pressure risk assets, while falling real rates support higher valuations and economic activity.

ICE BofA US High Yield Spread

BAMLH0A0HYM2

· FRED

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 3.19% |

+0.0% |

-0.9% |

+7.4% |

+12.7% |

As of March 24, 2026

Option-adjusted spread of US high yield corporate bonds over Treasuries.

The price of credit risk. Below 3% = euphoria, risk underpriced. 3-5% = normal. Above 5% = stress building. Above 8% = crisis-level credit distress.

US Equities

S&P 500 Equal Weight

RSP

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $192.85 |

+$0.93 (+0.5%) |

+$0.20 (+0.1%) |

$-9.74 (-4.8%) |

+$0.81 (+0.4%) |

As of March 25, 2026

Equal-weighted version of the S&P 500, removing concentration in mega-cap stocks.

This helps assess market breadth; if it lags the standard index, it indicates narrow leadership, while outperformance signals broad participation across stocks.

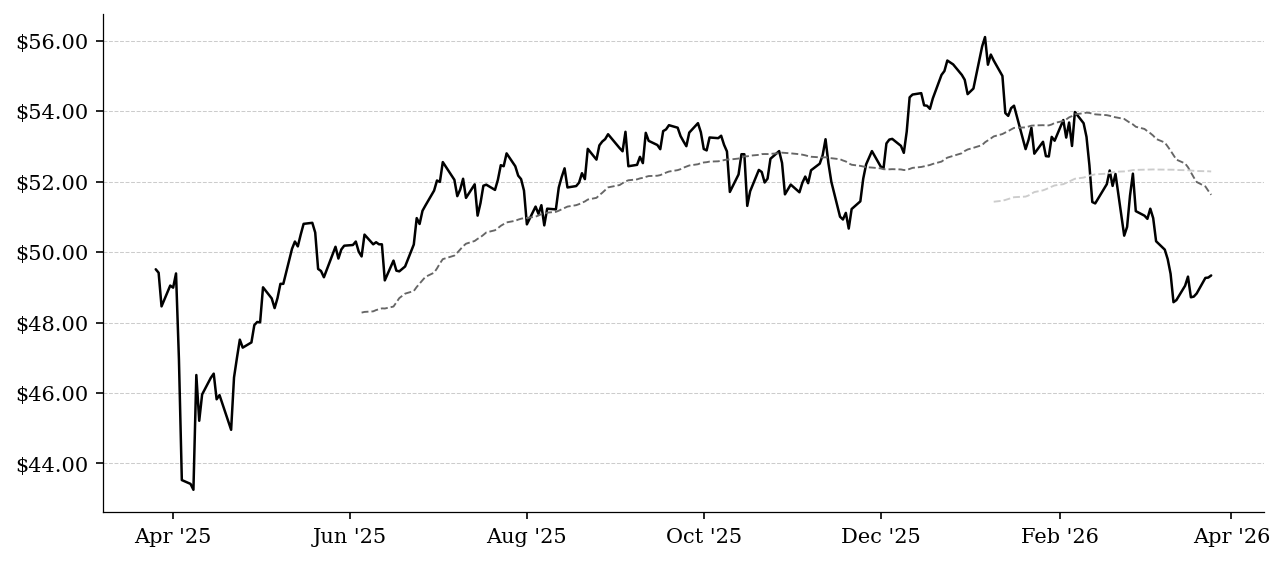

Financial Select Sector SPDR

XLF

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $49.34 |

+$0.06 (+0.1%) |

+$0.62 (+1.3%) |

$-1.38 (-2.7%) |

$-5.31 (-9.7%) |

As of March 25, 2026

ETF tracking U.S. financial institutions including banks and insurers.

Financials are highly sensitive to rates and credit conditions; strength suggests healthy lending and economic expansion, while weakness can signal tightening credit or stress in the financial system.

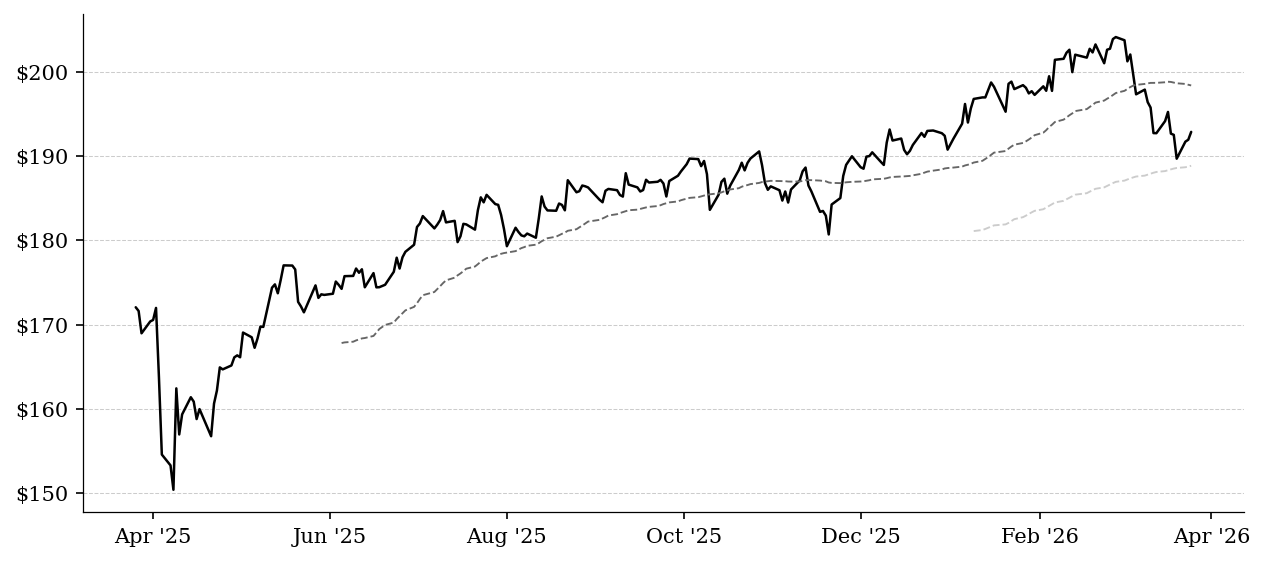

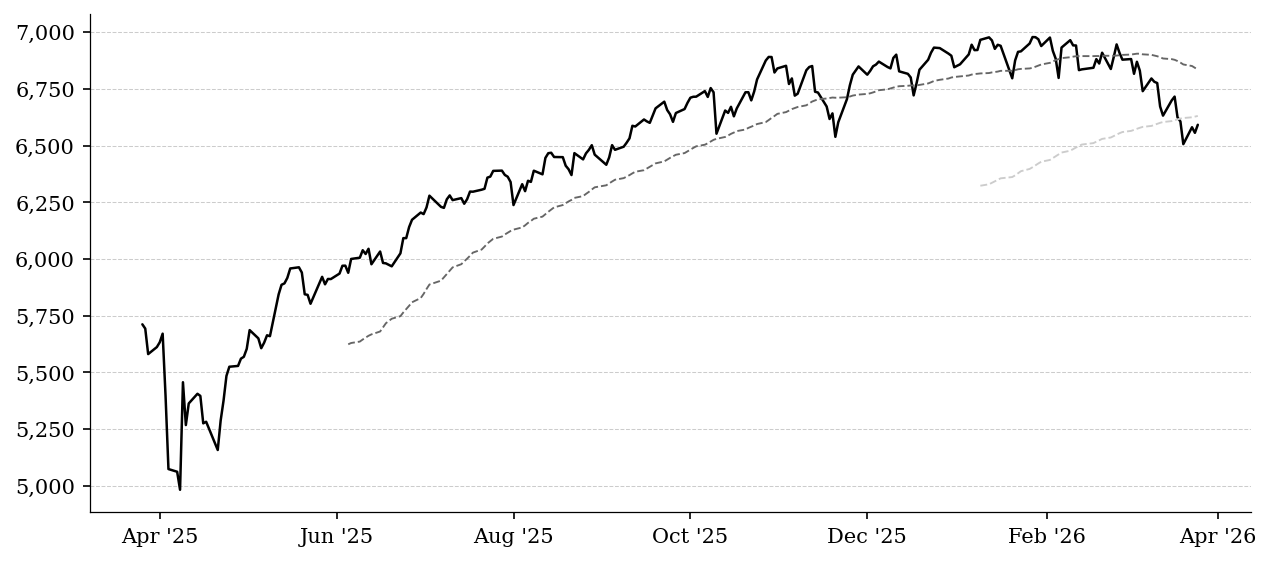

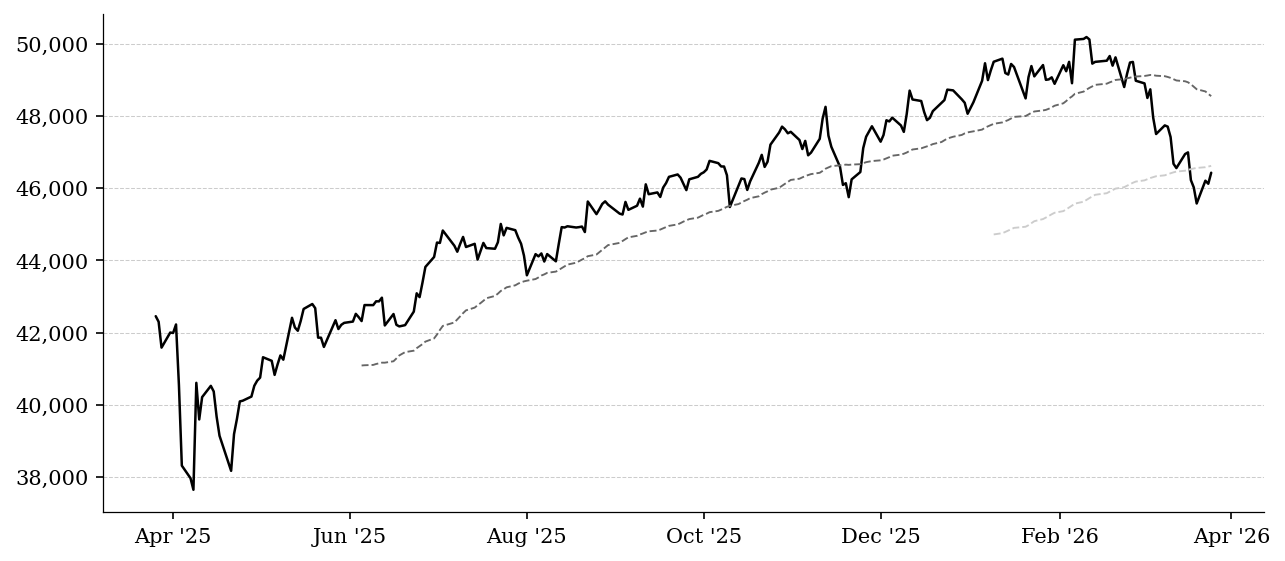

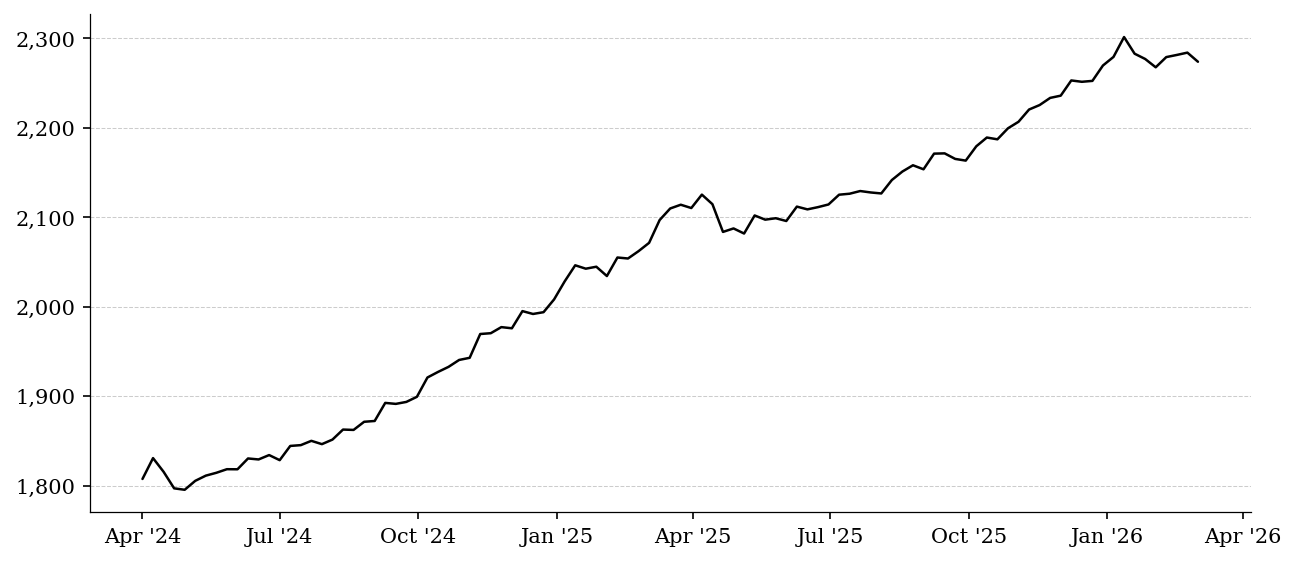

S&P 500

^GSPC

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 6,591.90 |

+0.5% |

-0.5% |

-4.3% |

-3.9% |

As of March 25, 2026

Market-cap-weighted index of 500 large U.S. companies.

This is the primary benchmark for U.S. equities; movements reflect a combination of earnings expectations, interest rates, and risk appetite, making it a broad indicator of financial conditions.

Nasdaq Composite

^IXIC

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 21,929.83 |

+0.8% |

-1.0% |

-4.1% |

-5.6% |

As of March 25, 2026

Index heavily weighted toward technology and growth-oriented companies.

This is highly sensitive to interest rates and liquidity; outperformance typically signals strong risk appetite and falling discount rates, while underperformance often reflects tightening conditions.

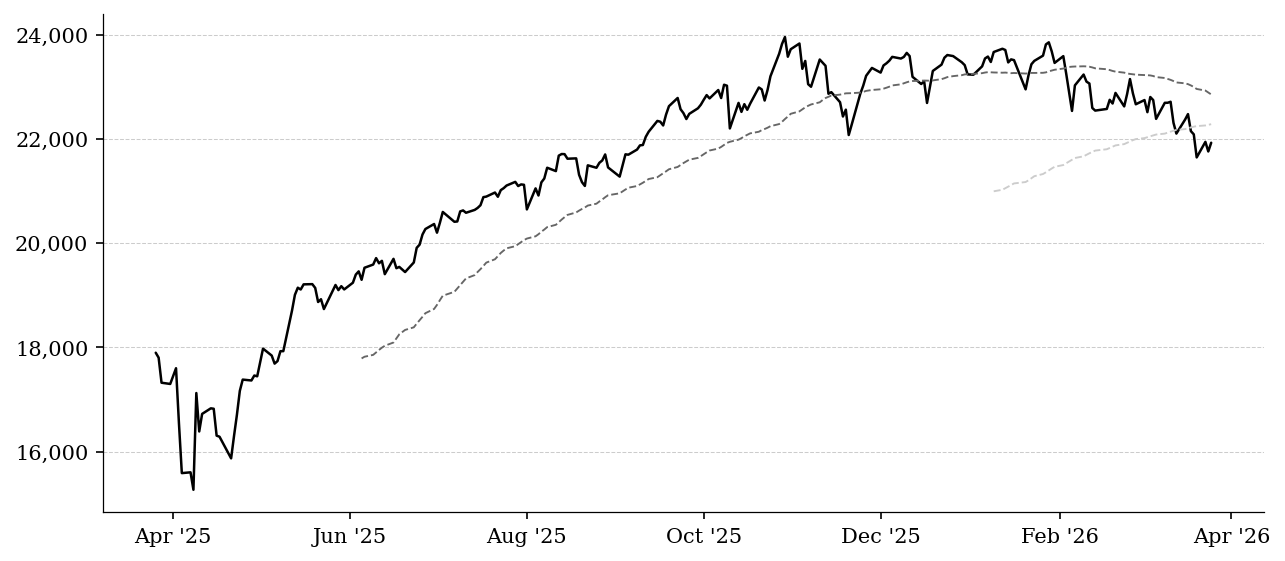

Dow Jones Industrial Average

^DJI

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 46,429.49 |

+0.7% |

+0.4% |

-5.6% |

-4.0% |

As of March 25, 2026

Price-weighted index of 30 large, established U.S. companies.

This tends to reflect more traditional, cyclical sectors and can provide a view into industrial and economic sensitivity relative to growth-heavy indices.

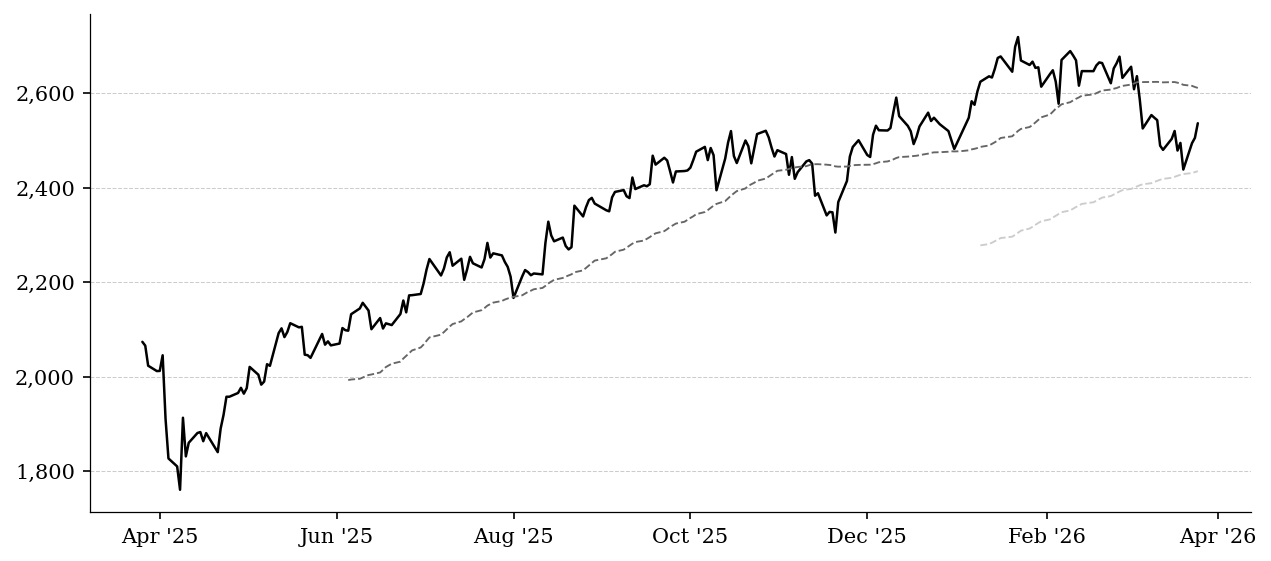

Russell 2000

^RUT

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 2,536.38 |

+1.2% |

+2.3% |

-4.4% |

+1.1% |

As of March 25, 2026

Index of small-cap U.S. companies.

This is a proxy for domestic economic strength and credit sensitivity; outperformance suggests strong growth and easy financial conditions, while weakness indicates stress in smaller, more leveraged businesses.

VIX

^VIX

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 25.33 |

-6.0% |

+1.0% |

+29.6% |

+74.6% |

As of March 25, 2026

Implied volatility of S&P 500 options, often called the "fear index."

Elevated levels indicate market stress and uncertainty, while low levels suggest complacency and stable conditions, making it a key barometer of risk sentiment.

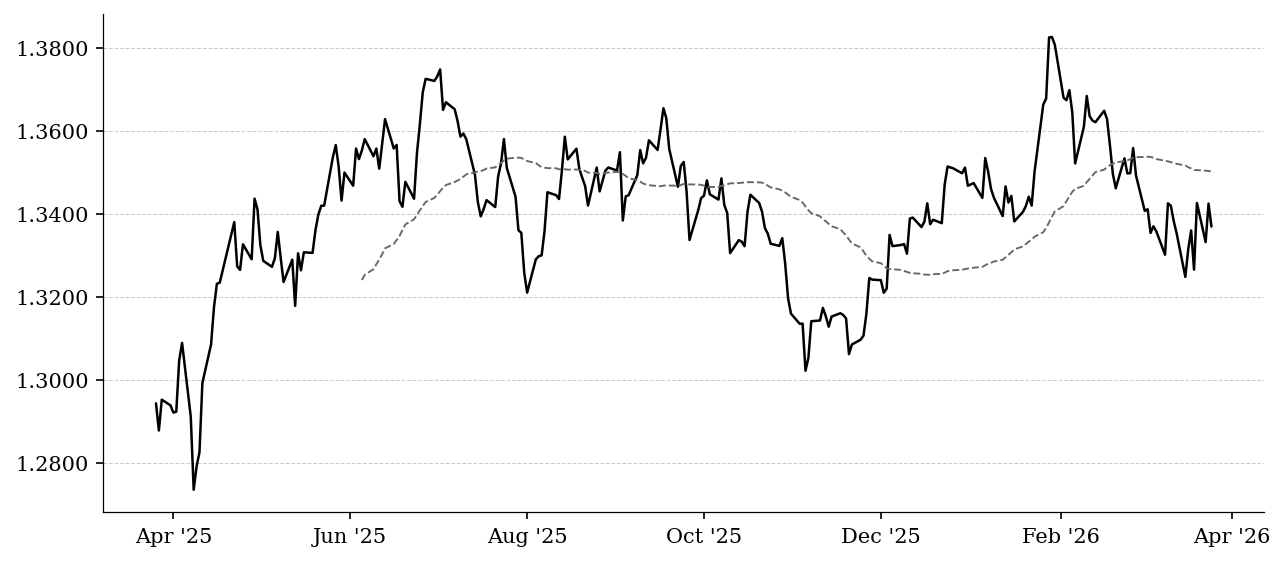

Currencies & Gold

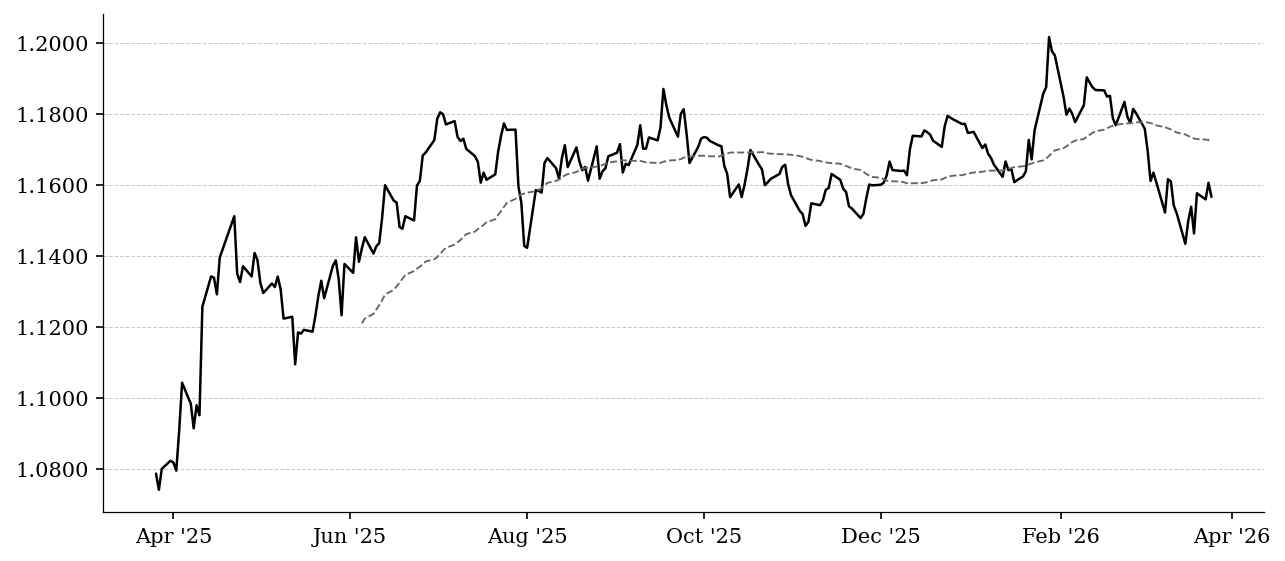

EUR/USD

EURUSD=X

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 1.1567 |

-0.3% |

+0.2% |

-1.9% |

-1.6% |

As of March 25, 2026

Exchange rate between the euro and U.S. dollar.

Reflects relative economic strength and monetary policy between the U.S. and Europe, often serving as a proxy for global macro positioning.

USD/JPY

JPY=X

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 159.3760 |

+0.6% |

+0.3% |

+3.1% |

+1.7% |

As of March 25, 2026

Exchange rate between the U.S. dollar and Japanese yen.

Highly sensitive to interest rate differentials; a rising pair typically reflects higher U.S. yields and global carry trades, while declines often occur during risk-off periods.

GBP/USD

GBPUSD=X

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 1.3369 |

-0.4% |

+0.1% |

-0.9% |

-0.8% |

As of March 25, 2026

Exchange rate between the British pound and U.S. dollar.

Reflects UK-specific economic conditions and policy relative to the U.S., with sensitivity to global risk sentiment.

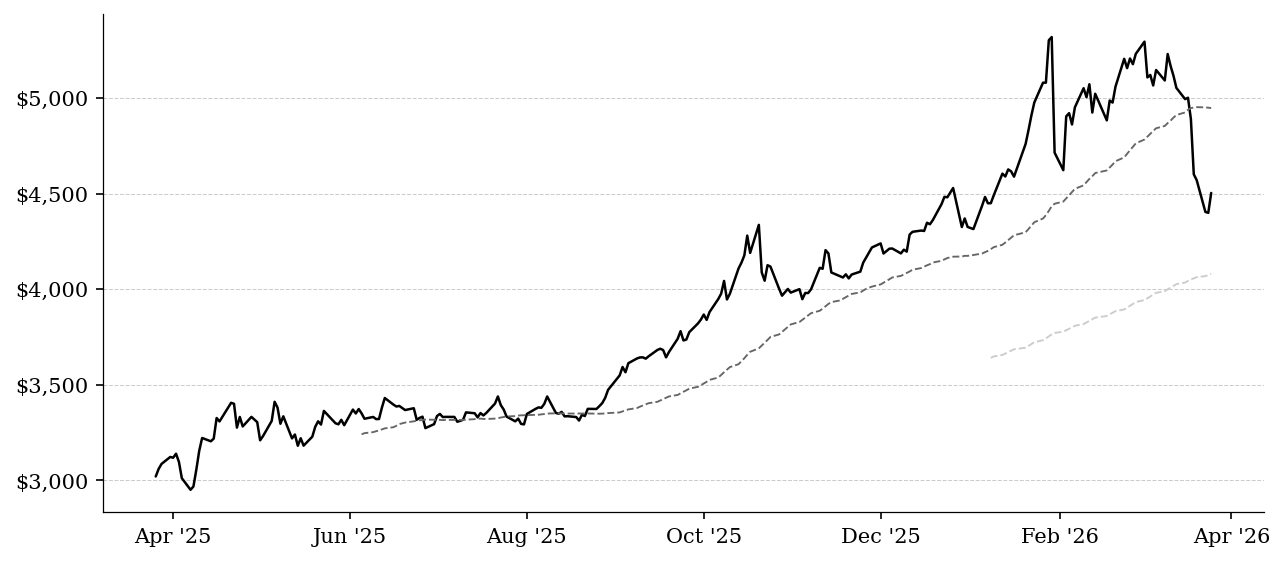

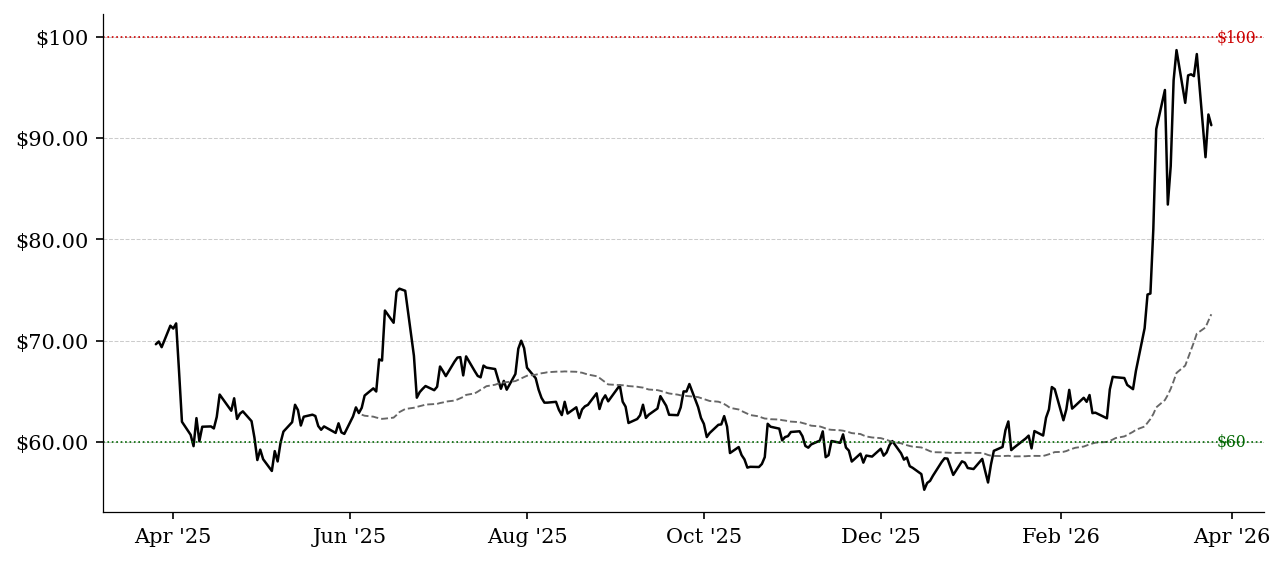

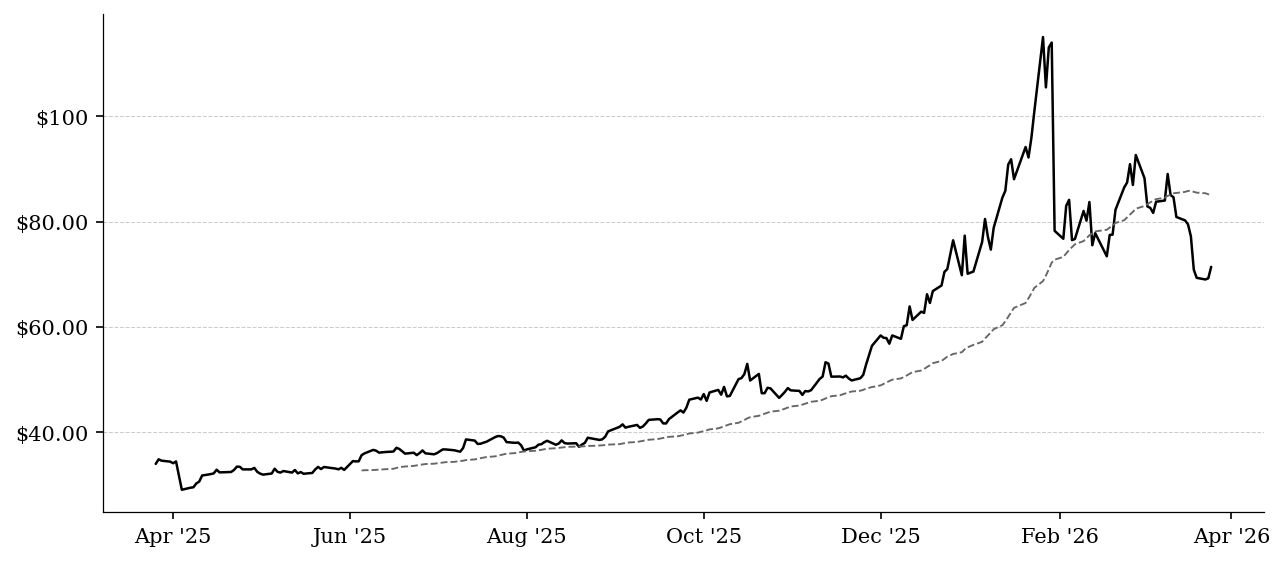

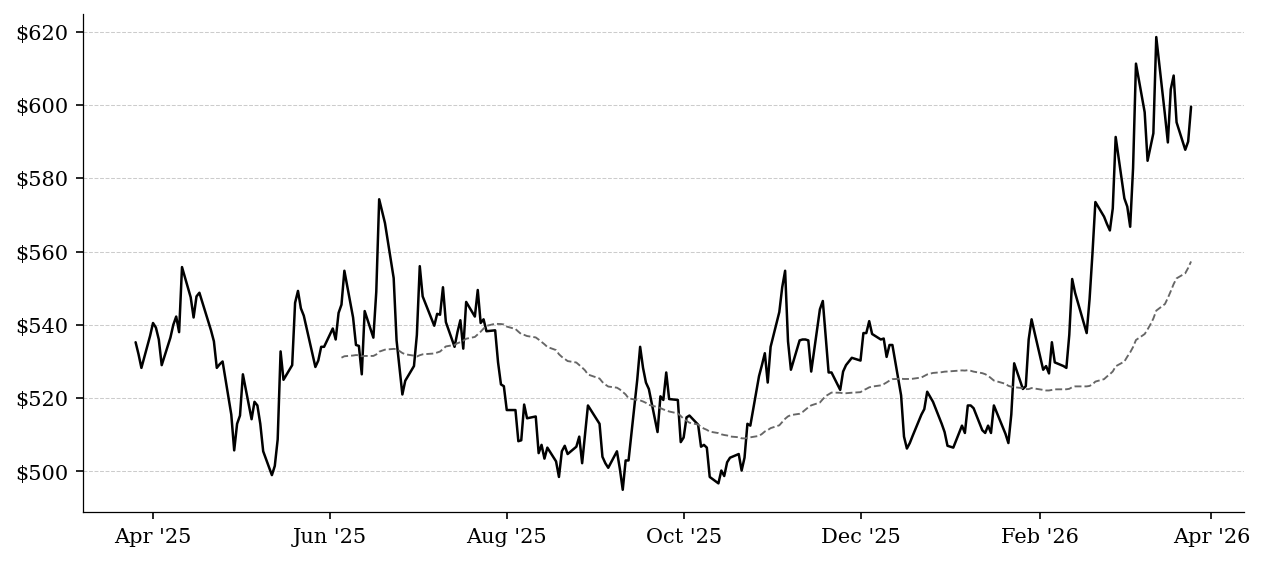

Gold

GC=F

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $4,503.30 |

+$104.00 (+2.4%) |

$-386.60 (-7.9%) |

$-652.50 (-12.7%) |

+$188.90 (+4.4%) |

As of March 25, 2026

Precious metal used as a store of value.

Typically rises during periods of declining real rates, inflation concerns, or geopolitical risk, serving as a hedge against monetary instability.

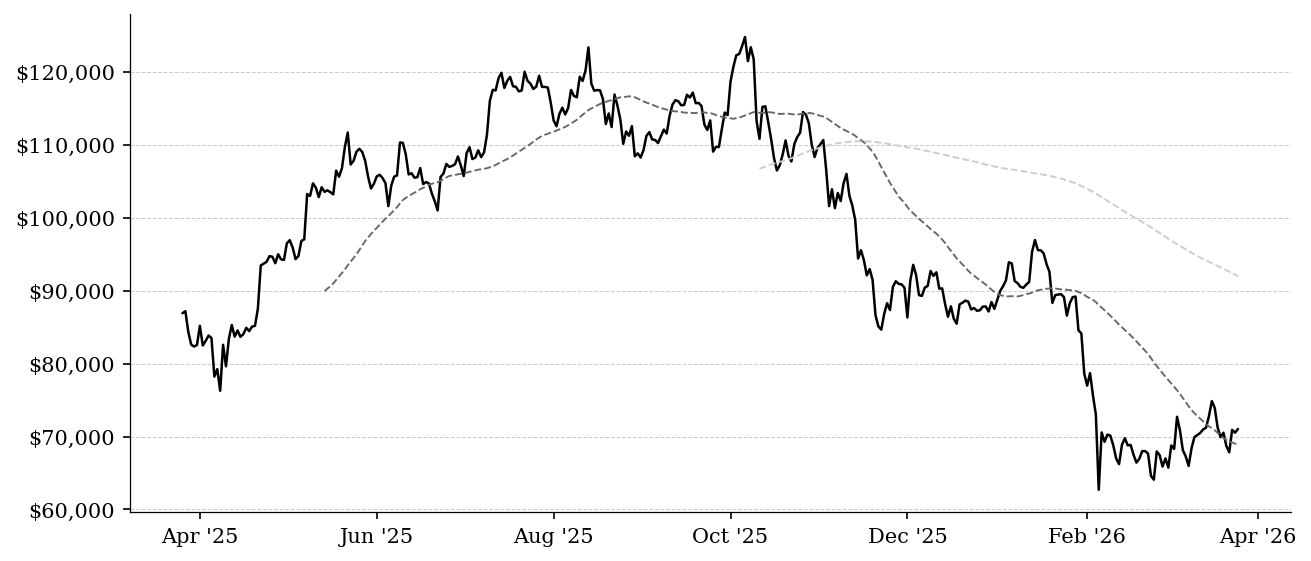

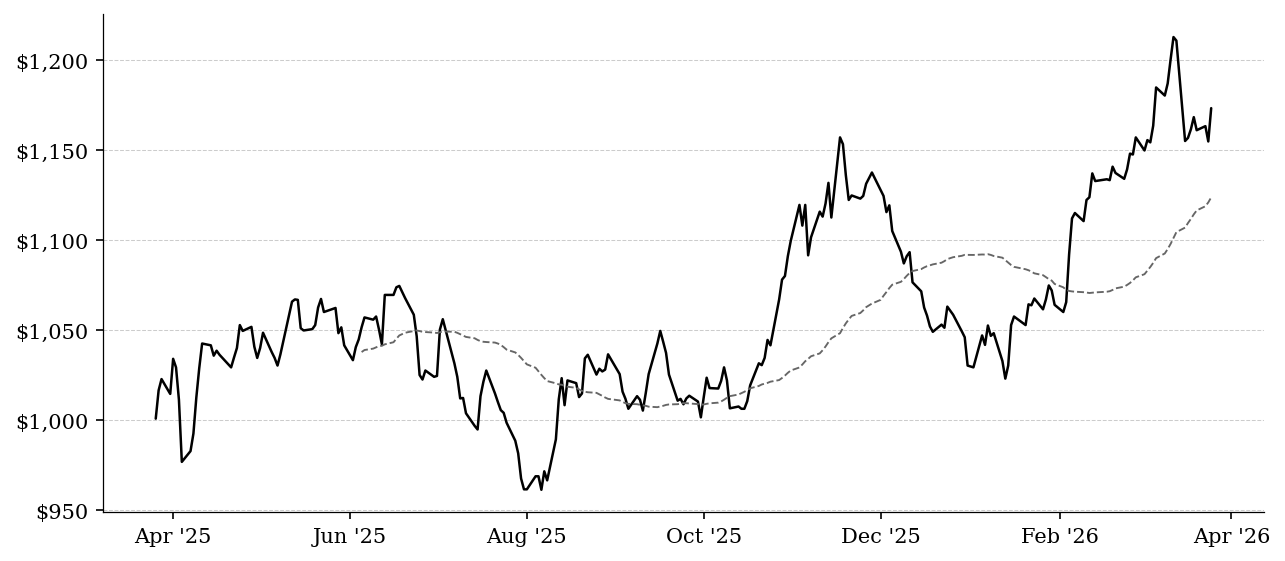

Bitcoin

BTC-USD

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $71,031.61 |

+$513.75 (+0.7%) |

+$509.02 (+0.7%) |

$-1,678.97 (-2.3%) |

$-17,700.38 (-19.9%) |

As of March 25, 2026

Digital asset often viewed as a speculative or alternative store of value.

Highly sensitive to liquidity and risk appetite; strong performance often coincides with easy financial conditions and speculative behavior.

Commodities

Crude Oil (WTI)

CL=F

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $91.29 |

$-1.06 (-1.1%) |

$-5.03 (-5.2%) |

+$25.66 (+39.1%) |

+$33.97 (+59.3%) |

As of March 25, 2026

Benchmark price for U.S. crude oil.

Rising oil prices can signal strong demand or supply constraints and tend to be inflationary, while falling prices often indicate weakening global growth.

Natural Gas

NG=F

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $2.94 |

$-0.00 (-0.1%) |

$-0.12 (-4.1%) |

+$0.03 (+0.9%) |

$-0.68 (-18.7%) |

As of March 25, 2026

Price of natural gas, a key energy input.

Often more supply-driven but still relevant for inflation and industrial activity, particularly in energy-sensitive regions.

Copper

HG=F

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $5.52 |

+$0.10 (+1.8%) |

$-0.03 (-0.6%) |

$-0.40 (-6.8%) |

$-0.12 (-2.1%) |

As of March 25, 2026

Industrial metal widely used in construction and manufacturing.

Often called "Dr. Copper," it is a leading indicator of global economic activity, with rising prices signaling growth and falling prices indicating slowdown.

Silver

SI=F

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $71.44 |

+$2.17 (+3.1%) |

$-5.79 (-7.5%) |

$-16.01 (-18.3%) |

+$0.89 (+1.3%) |

As of March 25, 2026

Silver futures. Industrial metal and precious metal hybrid.

Dual nature: industrial demand (solar, electronics) and safe-haven store of value. Outperforming gold = industrial optimism. Underperforming = pure fear bid favoring gold.

Soybeans

ZS=F

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $1,173.50 |

+$18.50 (+1.6%) |

+$11.75 (+1.0%) |

+$34.00 (+3.0%) |

+$144.00 (+14.0%) |

As of March 25, 2026

Soybean futures. Agricultural bellwether and food inflation proxy.

Key input for animal feed and cooking oil. Rising = food inflation pressure, supply disruption (weather, trade policy). Falling = bumper crops or demand destruction.

Wheat

ZW=F

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $599.50 |

+$9.50 (+1.6%) |

$-4.75 (-0.8%) |

+$32.00 (+5.6%) |

+$93.00 (+18.4%) |

As of March 25, 2026

Wheat futures. Global food security and geopolitical risk indicator.

Staple food commodity sensitive to weather, war, and trade restrictions. Spikes signal food inflation risk and geopolitical supply disruption.

Institutional Flows

Fed Balance Sheet Total Assets

WALCL

· FRED

· Weekly

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 6,655,939.00 |

+0.1% |

+0.5% |

+1.0% |

+1.3% |

As of March 18, 2026

Federal Reserve total assets in millions. Proxy for liquidity injections.

Rising = Fed expanding balance sheet, adding liquidity, supportive for risk assets. Falling = quantitative tightening, draining liquidity, headwind for all asset prices.

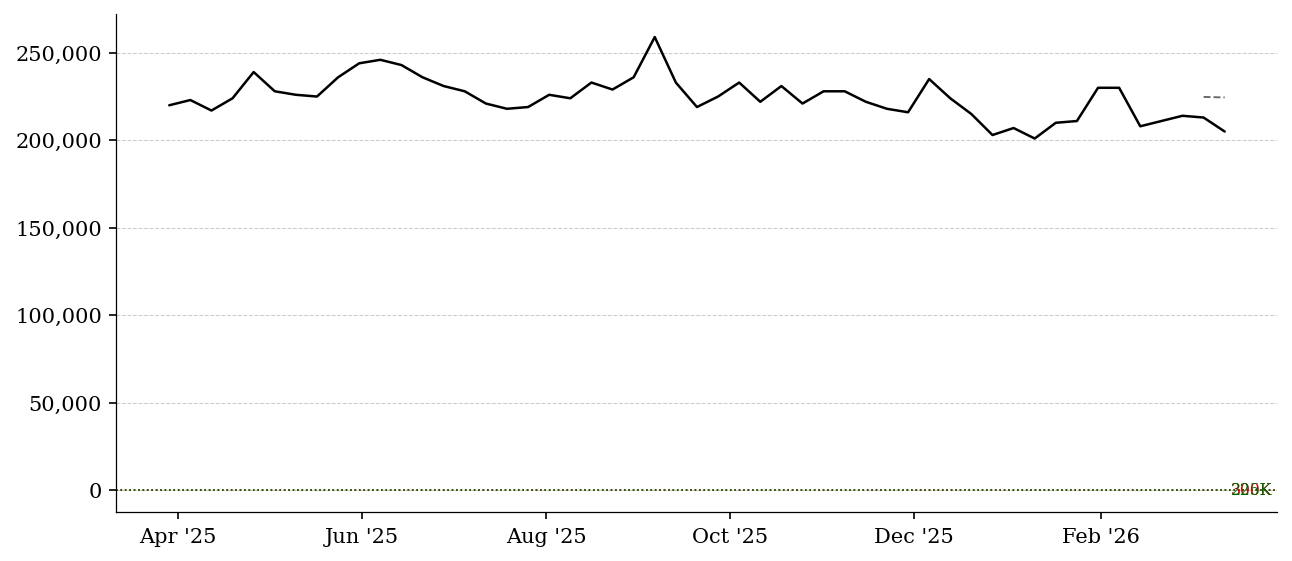

Initial Jobless Claims

ICSA

· FRED

· Weekly

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 205,000.00 |

-3.8% |

-10.9% |

-11.3% |

-1.0% |

As of March 14, 2026

Weekly new unemployment insurance claims in thousands.

The fastest labor market pulse. Below 225K = tight labor market. Rising trend above 300K = layoffs accelerating, recession risk climbing.

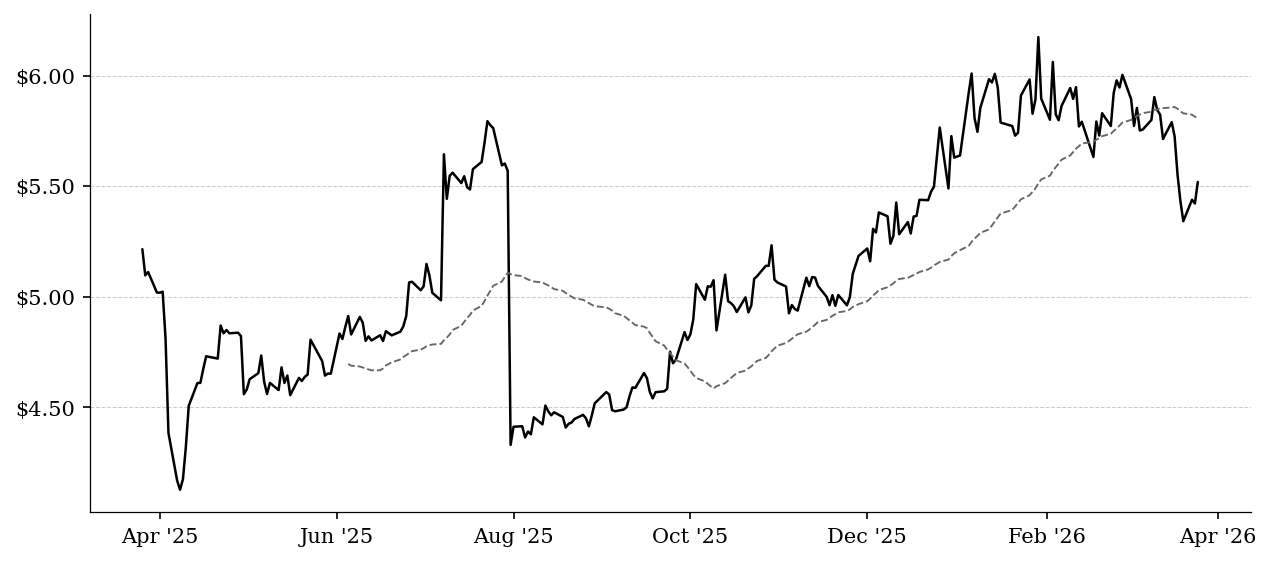

iShares TIPS Bond ETF

TIP

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $110.16 |

+$0.33 (+0.3%) |

$-1.08 (-1.0%) |

$-1.15 (-1.0%) |

+$0.30 (+0.3%) |

As of March 25, 2026

TIPS ETF. Proxy for inflation protection demand.

Rising = investors buying inflation protection, real yields falling. Falling = inflation fears fading or real yields rising and punishing duration.

Retail Money Market Funds

WRMFNS

· FRED

· Weekly

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 2,273.90 |

-0.4% |

-0.1% |

+4.3% |

-0.2% |

As of March 2, 2026

Retail money market fund assets in billions. Cash on the sidelines.

Record highs = massive cash parked defensively, potential fuel for future equity rally. Falling = money moving out of cash into risk assets, bullish rotation underway.

Real Estate Proxies

Vanguard Real Estate ETF

VNQ

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $87.84 |

$-0.07 (-0.1%) |

$-3.15 (-3.5%) |

$-6.28 (-6.7%) |

+$0.26 (+0.3%) |

As of March 25, 2026

ETF tracking publicly traded U.S. real estate investment trusts.

Reflects the impact of rates and economic conditions on real estate valuations, often acting as a liquid proxy for private market trends.

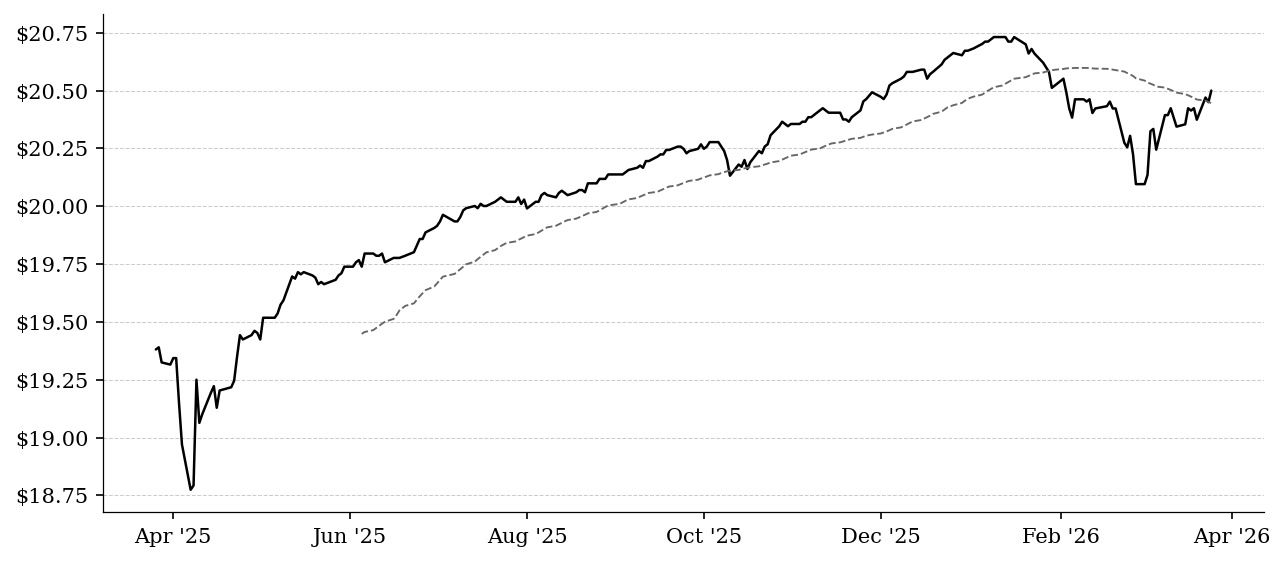

SPDR Homebuilders ETF

XHB

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $100.56 |

+$0.87 (+0.9%) |

+$1.20 (+1.2%) |

$-16.39 (-14.0%) |

$-3.75 (-3.6%) |

As of March 25, 2026

ETF tracking U.S. homebuilding companies.

Highly sensitive to mortgage rates and housing demand, providing a forward-looking view on residential real estate activity.

iShares MBS ETF

MBB

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $94.73 |

+$0.50 (+0.5%) |

$-0.25 (-0.3%) |

$-1.49 (-1.6%) |

+$0.24 (+0.3%) |

As of March 25, 2026

ETF representing mortgage-backed securities.

Reflects conditions in mortgage financing markets; weakness often indicates widening spreads and tighter housing finance conditions.

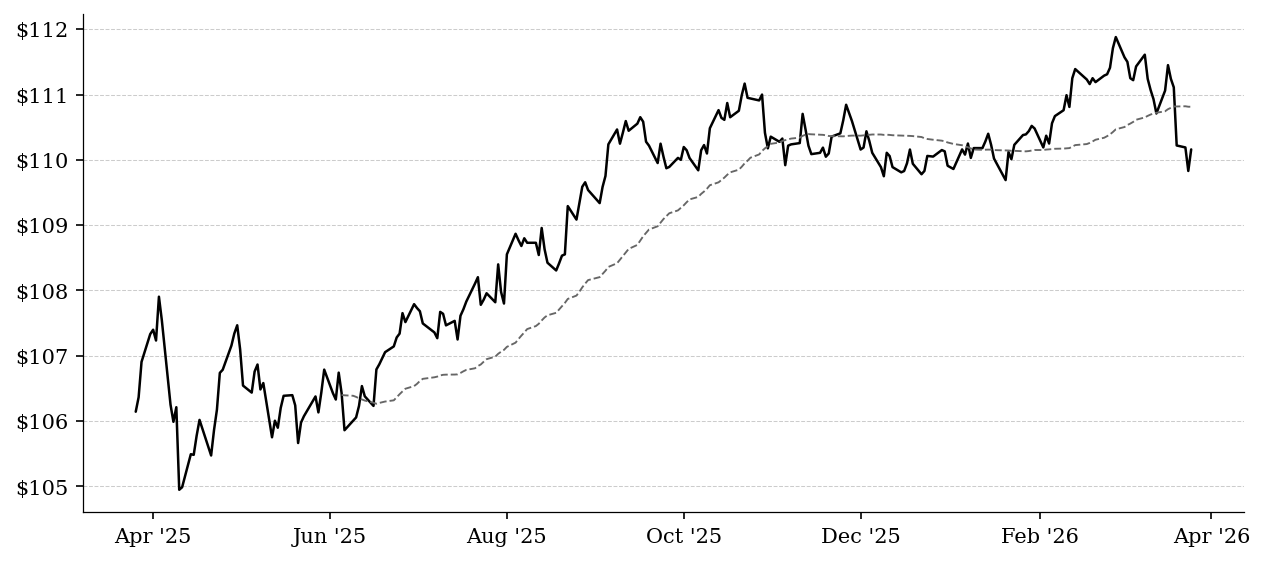

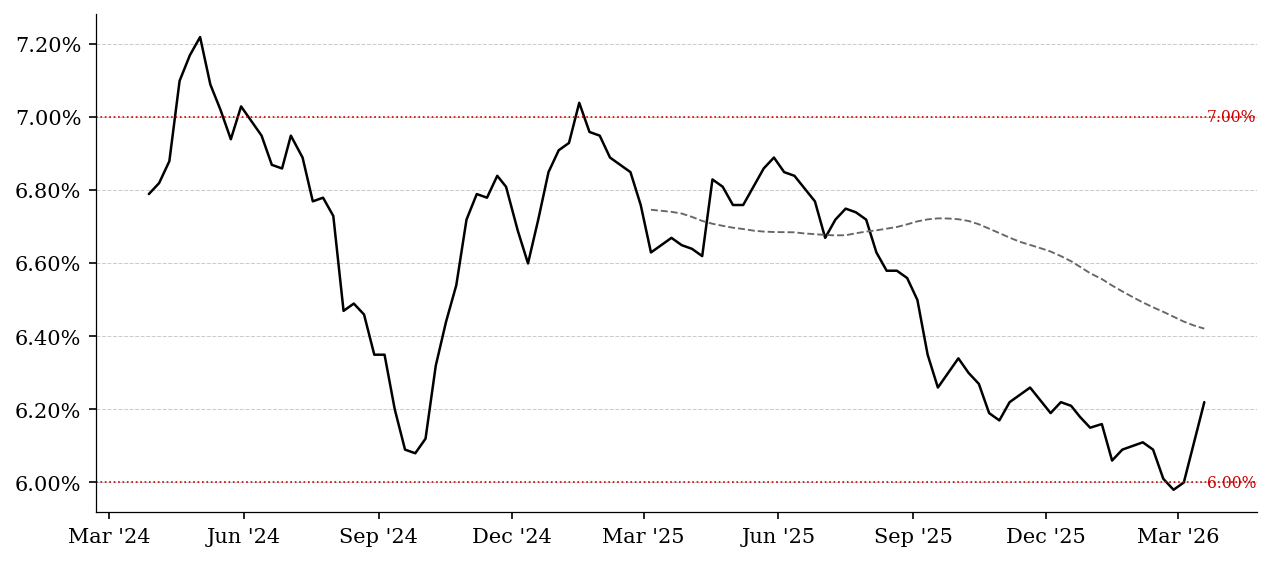

30Y Fixed Mortgage Rate

MORTGAGE30US

· FRED

· Weekly

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 6.22% |

+1.8% |

+2.1% |

+0.5% |

+1.0% |

As of March 19, 2026

Freddie Mac 30-year fixed-rate mortgage average.

The rate that drives housing affordability. Above 7% = demand destruction. Below 6% = refis restart and buyers return. Every 1% move reprices monthly payments ~10%.

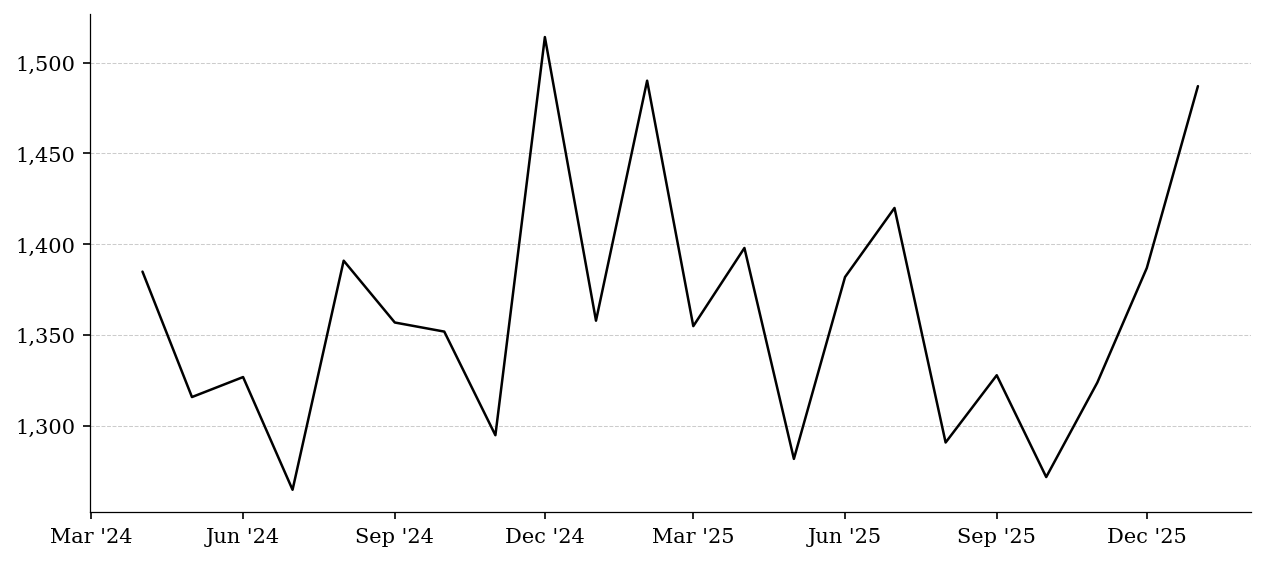

Housing Starts

HOUST

· FRED

· Monthly

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 1,487.00 |

+7.2% |

+15.2% |

+7.4% |

N/A |

As of January 1, 2026

New residential construction starts in thousands of units.

Leading indicator of housing supply and builder confidence. Rising = builders see demand. Falling = rates or costs choking new construction.

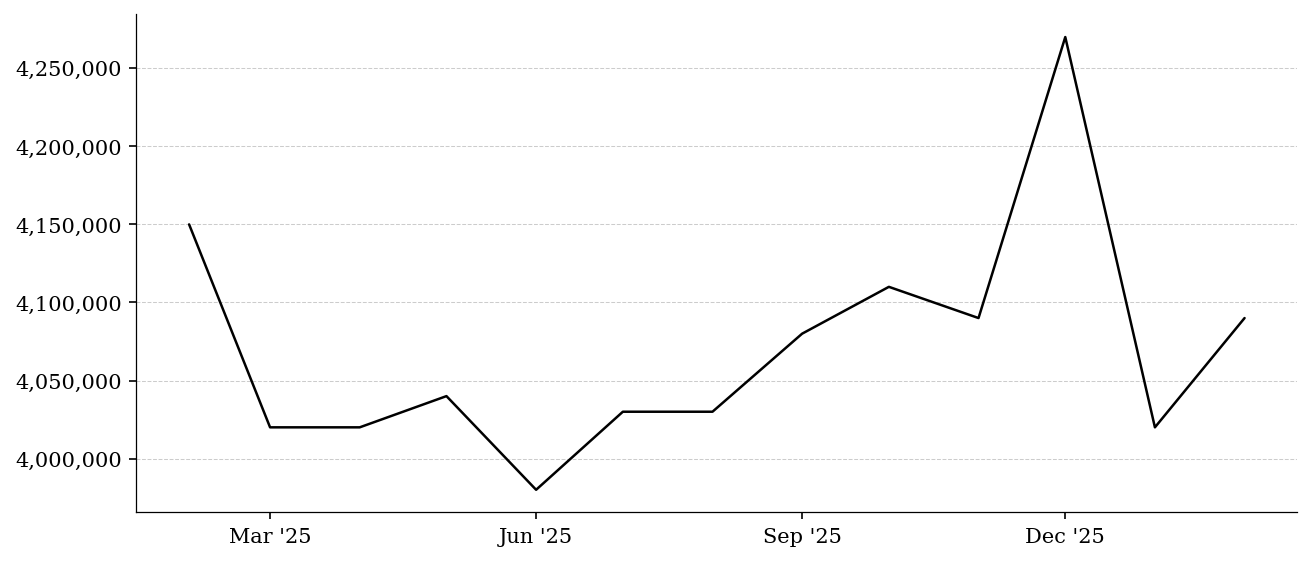

Existing Home Sales

EXHOSLUSM495S

· FRED

· Monthly

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 4,090,000.00 |

+1.7% |

+0.2% |

N/A |

+1.7% |

As of February 1, 2026

Existing home sales in millions of units annualized.

Volume indicator for the resale market. Falling = lock-in effect as owners hold low-rate mortgages. Rising = rate relief thawing the frozen housing market.

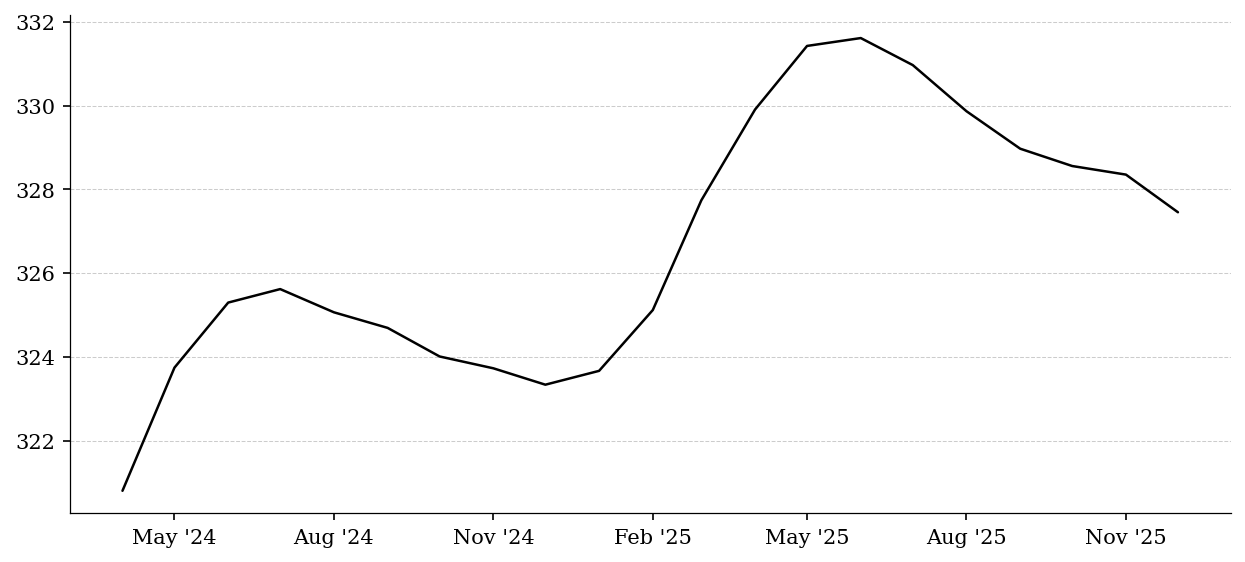

S&P/Case-Shiller Home Price Index

CSUSHPINSA

· FRED

· Monthly

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 327.45 |

-0.3% |

-1.1% |

+3.3% |

N/A |

As of December 1, 2025

National home price index. The definitive measure of US house prices.

The gold standard for home price trends. Rising = wealth effect for homeowners, affordability squeeze for buyers. Falling = negative equity risk, consumer retrenchment.

Building Permits

PERMIT

· FRED

· Monthly

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 1,376.00 |

-5.4% |

+3.5% |

-5.7% |

N/A |

As of January 1, 2026

New privately-owned housing units authorized in thousands.

Leading indicator — permits precede starts by 1-2 months. Rising = pipeline building, builder optimism. Falling = future supply contraction ahead.

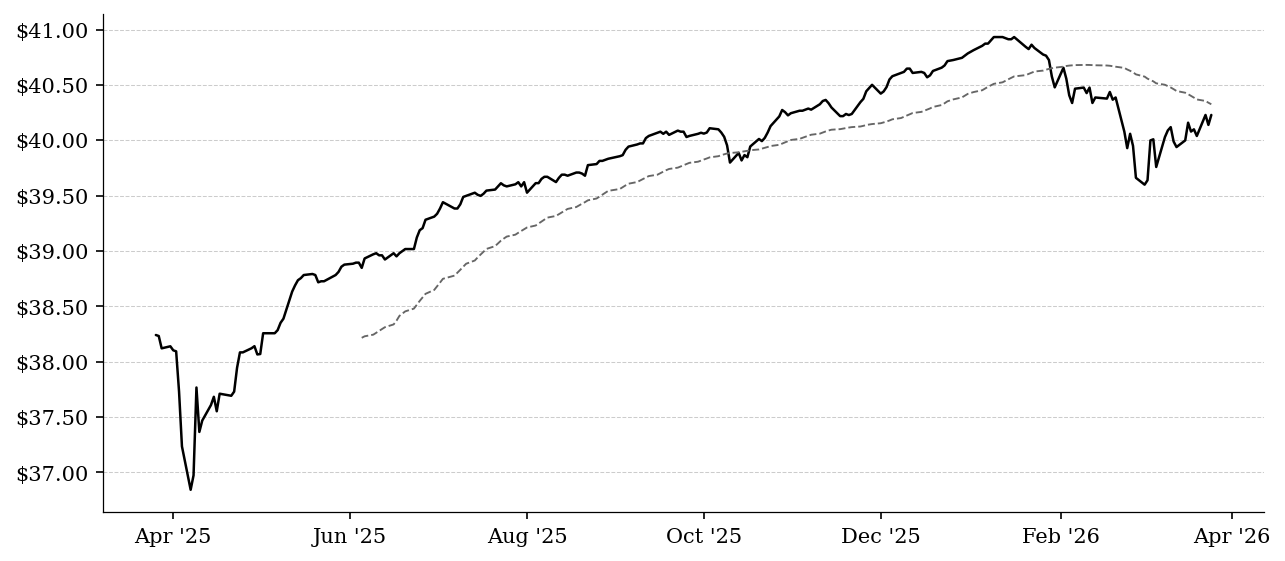

Private Credit

Senior Loans / Leveraged Loans (BKLN)

BKLN

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $20.50 |

+$0.05 (+0.2%) |

+$0.09 (+0.4%) |

+$0.25 (+1.2%) |

$-0.18 (-0.9%) |

As of March 25, 2026

Tracks leveraged loans (floating-rate senior secured). Core of private credit collateral.

The canary in private credit. Falling prices = stress in leveraged borrowers and CLOs. Floating-rate means rising rates hit these borrowers first.

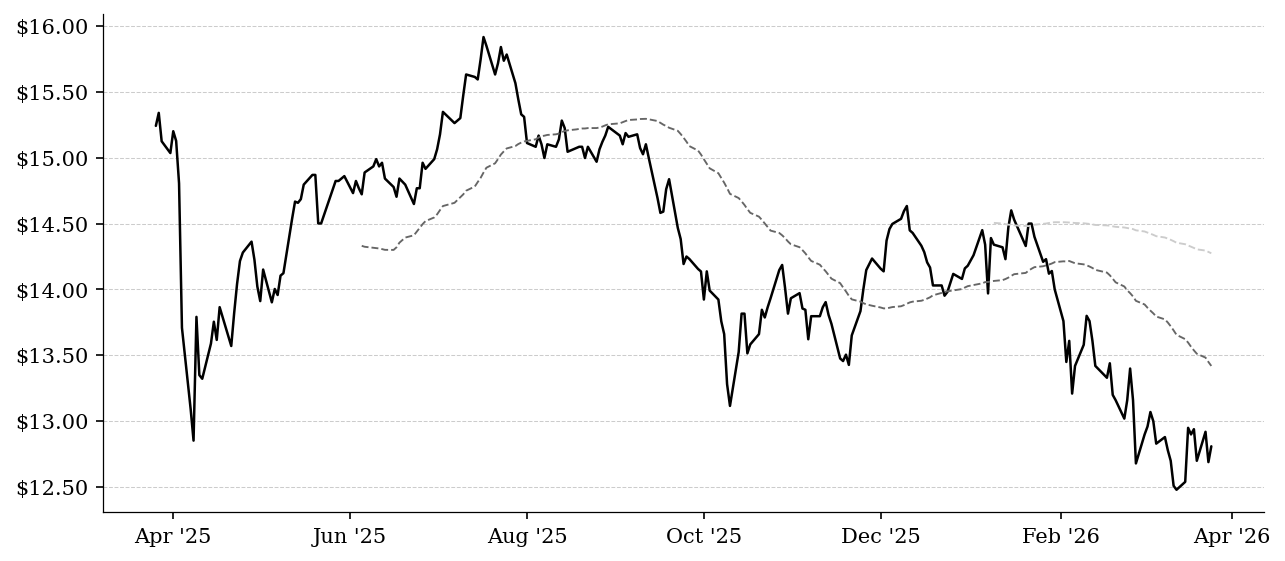

Business Development Companies (BIZD)

BIZD

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $12.81 |

+$0.12 (+0.9%) |

$-0.09 (-0.7%) |

$-0.35 (-2.7%) |

$-1.45 (-10.2%) |

As of March 25, 2026

ETF of publicly traded BDCs — the closest public proxy for private direct lending.

BDCs are the public window into private credit. Falling BIZD = rising defaults or NAV markdowns in direct lending portfolios. Discount to NAV widens when credit stress builds.

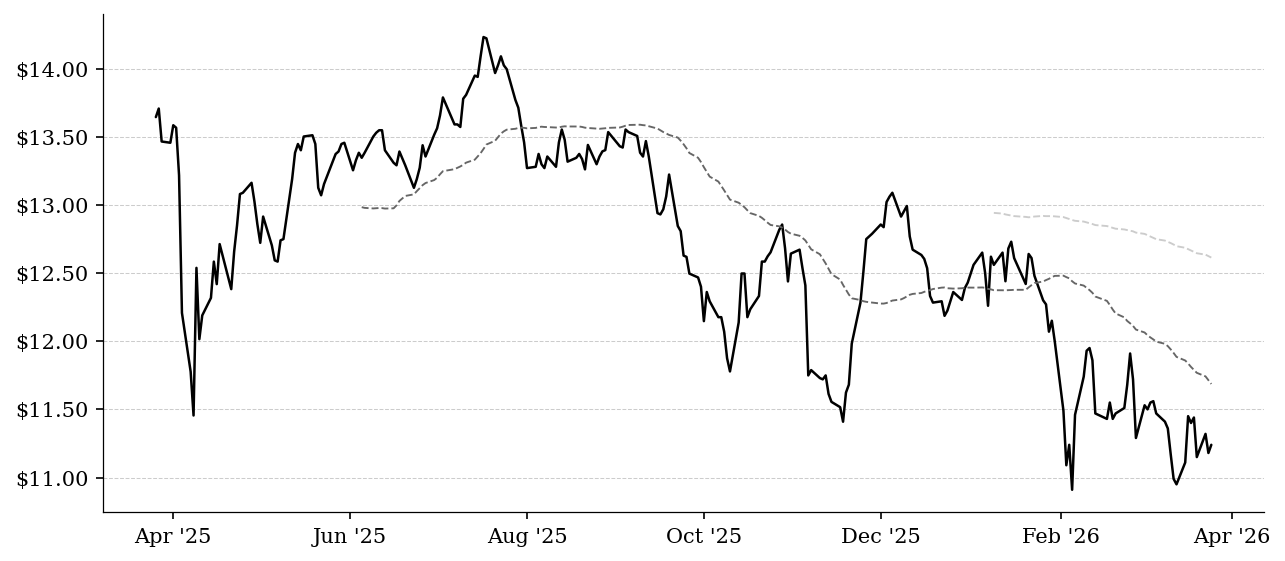

Blue Owl Capital Corporation (OBDC)

OBDC

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $11.24 |

+$0.06 (+0.5%) |

$-0.16 (-1.4%) |

$-0.44 (-3.8%) |

$-1.32 (-10.5%) |

As of March 25, 2026

Largest publicly traded direct lending BDC. Blue Owl's flagship private credit vehicle.

OBDC is the single best public read on private credit health. Price vs NAV discount signals market confidence in direct lending book values. Widening discount = market doubts marks on underlying loans.

Actively Managed Senior Loans (SRLN)

SRLN

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| $40.23 |

+$0.09 (+0.2%) |

+$0.15 (+0.4%) |

+$0.30 (+0.8%) |

$-0.59 (-1.4%) |

As of March 25, 2026

Actively managed leveraged loan fund. Complements BKLN with a manager-selected view.

When SRLN diverges from BKLN, active managers are seeing something passive indexing misses. Watch for widening gap during stress.

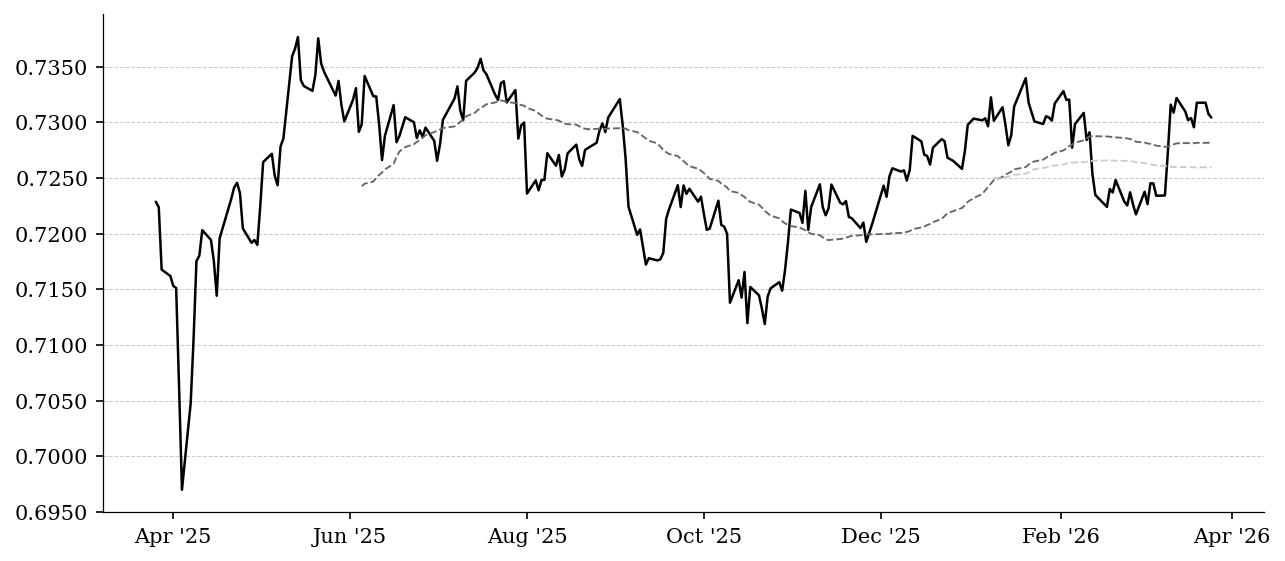

HY / IG Spread Proxy (HYG÷LQD)

HYG

· YAHOO

· Daily

| Current |

1 Day |

1 Week |

1 Month |

YTD |

| 0.7304 |

-0.0% |

+0.0% |

+1.1% |

+0.0% |

As of March 25, 2026

Ratio of high-yield to investment-grade bond ETFs. Proxy for credit spread direction.

Rising ratio = credit spreads tightening, risk appetite healthy. Falling ratio = spreads widening, stress migrating from junk toward quality.

56 Maple is a Chicago-based family office and investment platform focused on long-term capital deployment across real estate, private operating companies, as well as sponsor-led transactions. Rooted in a multigenerational real estate background, the firm partners with operators and sponsors to invest in cash-flowing assets and businesses with strong fundamentals. 56 Maple emphasizes disciplined underwriting, aligned incentives, and a long-term ownership mindset.